67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

Excerpt from GMO Quarterly Letter 2Q 2021: Dispelling Myths in the Value vs. Growth Debate

While there is no particular magic about 10x sales being the unique true sign of overvaluation, it has gained a certain amount of fame from a statement that Scott McNealy, co-founder and CEO of Sun Microsystems, made to Bloomberg in 2002:

…2 years ago we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?9

It is not strictly impossible for a stock trading at 10x sales or more to give a good return. Amazon was trading at well over 10x sales in the fall of 1999, and the return from then has been a very healthy 18% annualized, or 38x total gain over 22 years.10 On the other hand, Amazon did fall by almost 93% from that peak to the low 2 years later, and an investor who had held off and only bought when its price/sales fell below 10 in late 2000 would have made 89x his initial investment and saved himself a good deal of initial pain.11

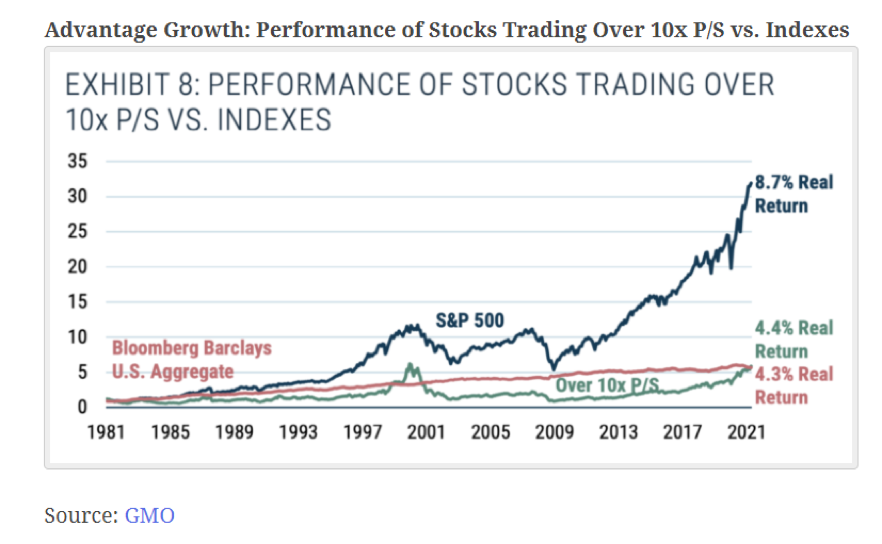

But the more important point is that the odds are strongly against companies trading at over 10x sales. Exhibit 8 shows the long-term real returns to a portfolio of stocks trading at 10x sales or more against the overall stock market.

9 “A Talk with Scott McNealy,” Bloomberg, March 31, 2002.

10 Return from November 1, 1999 to July 1, 2021 was 18.4% annualized as per Yahoo Finance.

11 Amazon fell a lot more between the fall of 2000 and the fall of 2001, and its valuation by the bottom was pretty pedestrian. The truly prescient investor who got in at the bottom and held all the way up would have made an even more mouthwatering 557x gain, but they were buying in at around 1x sales, a valuation even a value manager could love

Source: GMO LLC

This information is provided by LVW Advisors for general information and educational purposes based upon publicly available information from sources believed to be reliable – LVW Advisors cannot assure the accuracy or completeness of these materials. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. The information in these materials may change at any time and without notice. Past performance is not a guarantee of future returns.