67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

By Joseph Zappia, CCO/Co-CIO

Key takeaways:

- Dividend-paying stocks face pressure on many fronts today.

- Fundamental research and diversification are the keys to investing in income-oriented companies.

- Given ultralow interest rates, dividend payouts remain a crucial source of investment income.

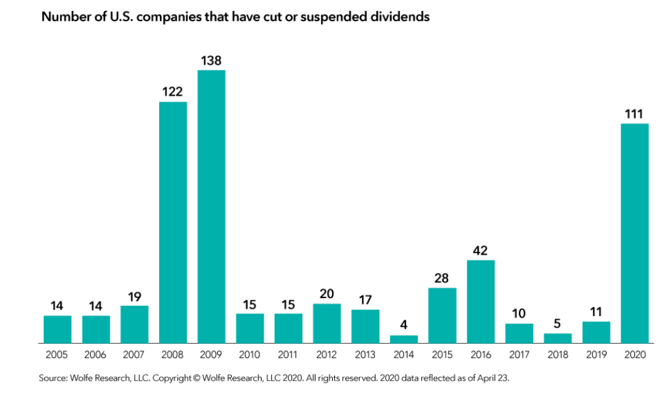

With much of the world in a stay-at-home lockdown, dividends are at a crossroads. As the global economy remains essentially shut down, many companies face tough choices when it comes to returning cash to shareholders. Dividend cuts and suspensions have jumped to the highest level in more than a decade. But even in this environment, some companies have maintained payouts and even raised them.

More than ever, this divergence in dividend commitment emphasizes the need for stock-specific research to help identify high-quality companies that can weather the storm. Interest rates also remain ultralow in developed markets, further underscoring the need to find companies that can generate sustainable income for investors who may be struggling to find it in bonds.

Dividends face challenges

In periods of economic duress, dividend cuts and suspensions are not unexpected. In the United States, they have reached a level last seen during the Great Recession, as sales have slowed and companies scramble to preserve cash. In Europe, dividends have come under immense political pressure as government regulators warn banks to preserve capital amid the coronavirus pandemic.

Many investors may be surprised to learn the degree to which ethical and social considerations are influencing dividend policy in a wide range of industries. This is especially prevalent among companies in France, Spain, and Germany.

Many European companies have delayed annual meetings to reevaluate conditions later this year. Given that some companies in Europe pay dividends only once or twice a year, instead of quarterly, the monetary impact and uncertainty is significant. Amid plummeting oil prices, Royal Dutch Shell on April 30 reduced its dividend for the first time since 1945, cutting it by more than 60% to 16 cents a share.

Rays of hope

Despite a severe global economic downturn, not all companies are following the same path. Many remain committed to sustaining and even increasing their dividends.

For example, in Europe, Nestlé and Zurich Insurance accelerated plans to hold virtual annual meetings and committed to paying dividends as planned. German chemical giant BASF is sticking to its payout, and several utilities in the U.K. have expressed strong support for sustaining their dividends during this turbulent time.

Among U.S. companies, Procter & Gamble and Johnson & Johnson have raised their disbursements, and Starbucks is maintaining its dividend. Even in the hard-hit oil sector, ExxonMobil said on April 29 it would maintain its quarterly dividend despite reporting a $610 million first-quarter loss.

Assessing dividend sustainability

As companies take different paths, LVW’s investment analysts are rigorously scrutinizing balance sheet strength, financial conditions, and cash-flow outlooks on a company-by-company basis.

Take the U.S. communications services industry, for example. The industry has consolidated in recent years, making several companies both providers and distributors of content. This consolidation has had financial ramifications.

AT&T acquired DirecTV and, more recently, Time Warner. As a result, AT&T’s net debt rose to $150 billion and its earnings became more economically sensitive due to the cyclical nature of the advertising business. On the other hand, Verizon Communications has roughly $130 billion of net debt and less exposure to advertising. Verizon stock has yielded less than AT&T, but its dividend is perceived to be safer by the market.

Understanding a company’s income statement and balance sheet is more important now than ever before. According to Capital Group, “Our equity analysts collaborate with our fixed income team to evaluate the risk that a company may cut its dividend to avoid a credit rating downgrade. High levels of corporate debt could impact dividend sustainability.”

Also important is weighing subjective issues that could impact the dividend, such as:

- Acquisitions: Companies may prioritize acquisitions, buying smaller or weaker competitors for strategic reasons while valuations are distressed, and cutting dividends to accelerate debt repayment.

- C-suite changes: A recently appointed CEO or new chairperson of the board may not have the same level of commitment to past dividend policies.

- Board composition: Some board members may be executives of other companies who have cut dividends and may not have any qualms about doing it again.

Consider upgrading your portfolio

A new paradigm is emerging for dividend-paying stocks and, therefore, we believe it is important to upgrade the quality of income-oriented portfolios.

In our view, an effective approach involves:

- Diversification: Generating a disproportionate amount of income from a given sector or region can increase the risk of a severe reduction of dividend income. Companies in many sectors outside of traditional areas, such as technology and health care, now pay dividends. A global approach, where appropriate, also expands the pool of dividend-paying companies, providing further diversification.

- Fundamental research: Financial and liquidity analysis can help assess the ability of a company to pay its dividend in a variety of scenarios through collaboration with equity and fixed income analysts.

- Holistic perspective: This involves assessing myriad qualitative and subjective factors including any recent management changes, the composition of the board, and the company’s approach to M&A during a time of distress.

Sources:

Bloomberg; Capital Group May 15, 2020

This material is for informational purposes only, it is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed herein are based on economic and market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened about investments in developing countries. Small-company stocks entail additional risks, and they can fluctuate in price more than larger company stocks.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The MSCI ACWI is a free float-adjusted market capitalization-weighted index that is designed to measure equity market results in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indexes.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.