67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

Download a copy of this newsletter

Table of Contents

FOURTH QUARTER MARKET REVIEW: INFLATION CHANGES THE GAME

OUTLOOK: THE MARKET HAS SHIFTED

POSITIONING: A TIME FOR CONSTRUCTIVE CAUTION

LVW NEWS

Thank you for reading the winter 2022 edition of The Serious Investor. The fourth quarter of 2021 may have marked the end of an era. After 13 years of ultra-accommodative monetary policies, the Federal Reserve announced it was planning three interest-rate hikes in 2022 to bring down high inflation. In this issue, we unpack that change and what it means for our clients, and we explain why we are entering the new year constructively but cautiously.

Quick Take:

-

Facing fast-rising inflation, the Federal Reserve became more hawkish in the fourth quarter.

-

The economy’s growth slowed from its 2021 peak but remained strong.

-

The S&P 500 posted large gains, but many stocks struggled, especially the speculative stocks that had surged in recent years.

-

Risks have risen—particularly the risk that Fed tightening could send a slowing economy into recession—so we are entering 2022 positioned cautiously.

-

We believe dispersion in the markets has created a number of compelling opportunities, and we are seeking to invest in them through skilled, selective managers.

FOURTH QUARTER MARKET REVIEW: INFLATION CHANGES THE GAME

Inflation was the big economic story of the fourth quarter. A combination of massive consumer demand and compromised supply chains drove up prices to a degree not seen since the early 1980s, with the U.S. Consumer Price Index (CPI) jumping 7% in 2021.

The rise, following 12-month increases of 6.2% in October and 6.8% in November, challenged the notion that high inflation would be short-lived. So did the broadening of price increases, which spread from spikes in discrete niches, such as used cars, to increases on items such as electronics, furniture, electricity, rent.

This shift had enormous implications. For the first time in over a decade, fast-rising inflation threatened to force monetary policymakers to back off the throttle. The Federal Reserve started tapering its asset purchases and signaled three interest rate hikes in 2022, while the Bank of England enacted a surprise rate increase in December.

Fiscal spending also came into question in the fourth quarter. Key provisions of COVID-19 rescue packages expired, including the expanded child tax credit, while President Biden’s signature Build Back Better bill died in the Senate (though speculation remained that a revised bill might be hammered out early in 2022). Meanwhile, the delta and omicron variants of COVID-19 led to spikes in infections, contributing to labor shortages and supply-chain disruptions late in 2021.

Despite all these challenges, the economy maintained strong growth through the fourth quarter. The Atlanta Fed GDPNow estimates that real GDP grew 6.8%, the economy added 955,000 jobs, and the unemployment rate fell from 4.8% to 3.9%. Yet some cracks started to show: Retail sales missed expectations in November, and job growth decelerated in December.

The S&P 500 logged a gain of more than 10% for the fourth quarter. But the benchmark’s rise was powered almost entirely by a few huge growth stocks, such as Apple (up 22%) and Microsoft (19%). Many other stocks struggled. On the New York Stock Exchange at year-end, nearly three times as many stocks traded at new 52-week lows as at new 52-week highs. Small stocks on the whole lagged their larger counterparts, with the Russell 2000 small-cap index gaining just 1.8% for the quarter.

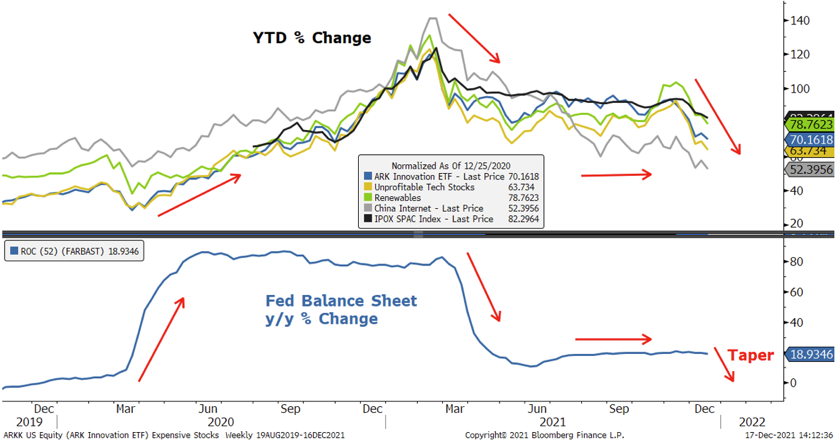

As liquidity declined, investors annihilated shares of more-speculative companies. The most expensive stocks in the S&P 500 fell almost 30% during the last two months of the year.1 The average stock on the Nasdaq dropped more than 20% from its peak—bear-market territory—and four in 10 stocks were down 50% or more, near a record.2 Although IPOs set volume and listing records for 2021 as a whole, many newly public stocks struggled mightily: As of late December, more than half of the year’s 481 new listings traded below their offer prices.3

Speculative stocks sell off amid less liquidity

OUTLOOK: THE MARKET HAS SHIFTED

It’s forecast season—the time of year when investing pros pretend they can predict what the economy and markets will do over the coming year. They invariably forecast returns near long-term averages, and they’re almost always wrong. In fact, the S&P 500’s total return was within three points of its average in just nine of the last 96 calendar years.4

That said, while history does not always repeat itself, markets tend to revert to the mean over time, so long-term averages are useful for helping us understand where we are on the playing field. The S&P 500 over the past 10 years has returned more than 17% annually, including dividends, about 40% higher than its long-term average.5 Mean reversion suggests returns will fall toward or below the average over the coming decade.

Valuations, growth and liquidity are the three pillars of our investment discipline, and they are in a very different place now than they were for most of the past decade. We remain constructive on the markets, but we believe the current environment calls for caution and an emphasis on skilled, selective managers rather than passive strategies.

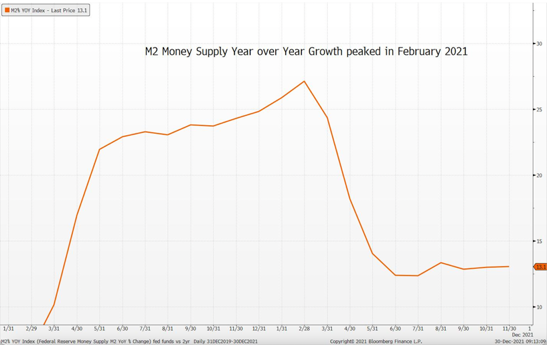

The tide of liquidity is ebbing

Plentiful liquidity has been the defining feature of the post-Great Recession era. It has helped support economic growth and push up asset prices since 2009, apart from a brief interruption at the beginning of the pandemic. We can’t take liquidity for granted anymore.

The Federal Reserve finds itself in an extraordinarily difficult position. Chair Jerome Powell and other members of the Fed seem to feel increased urgency to squash inflation by withdrawing some of the money sloshing around the economy, but they must try to accomplish that feat without tipping the economy into recession.

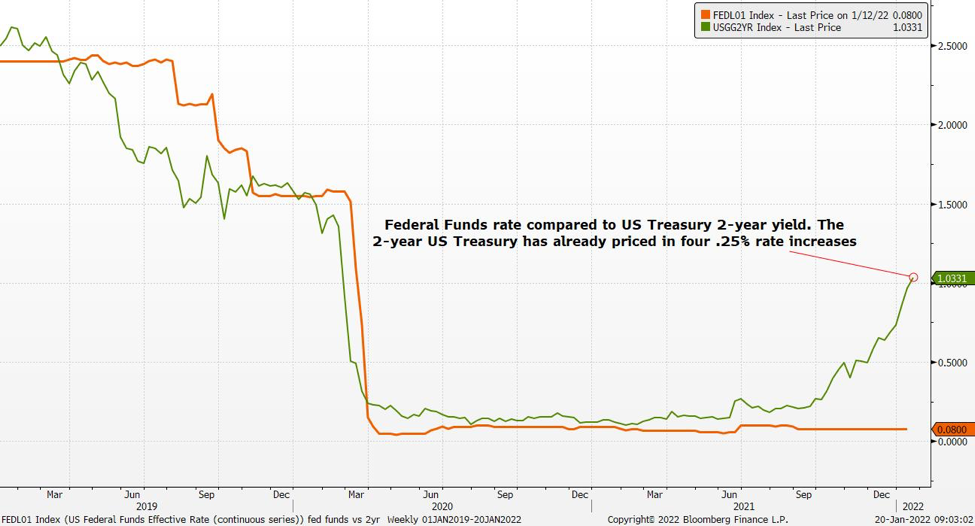

Liquidity already has fallen. In effect, tapering started early in 2021: The Fed had ballooned its balance sheet to support the financial system at the start of the pandemic, and that debt started to roll off in March and April.

Tapering is well underway

The equity market rotated and narrowed but didn’t collapse, alleviating fears that tapering might cause a stock market exodus. Still, we think investors should be careful not to underestimate the Fed’s determination to fight inflation. Powell historically has not been a dove on interest rates. Politically, he and the other members of the Fed must be keenly aware that the people who experience inflation most acutely tend to be those least able to afford it. And they face a backdrop in which under-investment in energy production has increased the risk of spikes in energy prices that could exacerbate broad-based inflation.

Reduced liquidity has changed dynamics in the markets. Treasury yields have climbed—not surprising, considering that inflation rose at its quickest pace in four decades. However, investors don’t appear to be selling bonds due to fears of inflation. Rather, they are betting the Fed will control prices with tighter policy. The shift in bond yields is affecting the mortgage lending market, with average rates for 30-year mortgages recently hitting two-year highs.6

Treasury yields jump

We noted above that speculative stocks have collapsed. If rates continue to rise, we’d expect the public markets to continue repricing expensive high-growth companies and the private markets to follow suit. We’re

We’re likely to see who’s been swimming naked, to paraphrase Warren Buffett. We expect volatility to climb, and problems may emerge in the financial system as debts become harder to finance. Tighter monetary policy also heightens the risk of recession and the potential for a severe correction.

In a key change from the past decade, inflation-related risks could tie the Fed’s hands if it needs to respond to new crises. The disinflationary backdrop since 2008 has allowed the Fed and other central banks to respond aggressively each time problems have arisen, then tighten slowly and predictably. If high inflation persists, the Fed may not be able to act so decisively to avert future crises.

Those conditions demand caution, so in the equity market we are emphasizing shares of companies that we believe are high quality and reasonably valued and entail defensive characteristics. All that said, the fact that a good deal of tightening is already priced into the bond market could give the Fed a bit more room to maneuver.

If inflation softens and policymakers see the need to support economic growth, the Fed may be able to pivot to a more dovish stance. Such a shift may not be sufficient to avert a full-blown crisis. But short of that scenario, a Fed pivot could help keep real interest rates negative, potentially helping stocks surprise on the upside over the coming months.

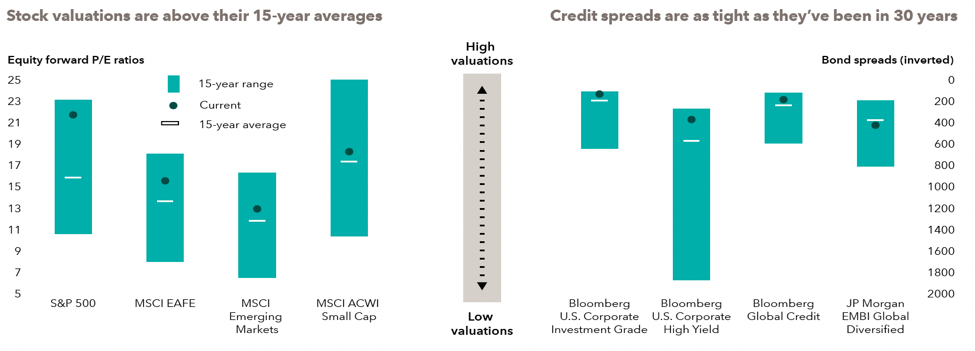

Benchmark valuations are high

The broad equity and credit markets are extremely expensive, and the S&P 500 looks especially rich.

Source: Capital Group, Bloomberg Index Services Ltd., IBES, J.P. Morgan, MSCI, Refinitiv Datastream, RIMES, Standard & Poor’s. As of 11/30/21. Bond spreads are the risk premium that investors receive for taking credit risk, and are calculated as the difference between bond yields and the risk-free rate.

Source: Capital Group, Bloomberg Index Services Ltd., IBES, J.P. Morgan, MSCI, Refinitiv Datastream, RIMES, Standard & Poor’s. As of 11/30/21. Bond spreads are the risk premium that investors receive for taking credit risk, and are calculated as the difference between bond yields and the risk-free rate.

Source: Callum Thomas Chart Storms, 12/20/21

As we have noted in many previous newsletters, high valuations historically have been associated with low future long-term returns. That said, the top heavy S&P 500 doesn’t accurately represent most of the stocks in the market. Apple, Microsoft, Amazon, Alphabet (Google), Tesla and Meta (Facebook) make up about a quarter of the S&P 500’s market capitalization, and their high prices pull up the index’s average valuation. Take Tesla, which recently traded at a price-to-earnings ratio over 330: Its more than $1 trillion market cap values the company at over $1 billion per vehicle sold.

The corrections in many other stocks have made their prices much more reasonable. Likewise, small caps are much less expensive than the S&P 500: The small-cap Russell 2000 Index traded at a 31% discount to its large-cap counterpart in late December, compared to a 22.5% discount over the past 13 years.

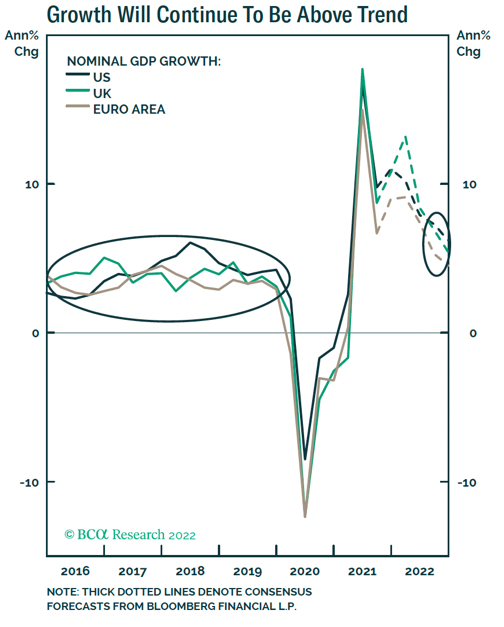

Growth likely to downshift

In our opinion, economic growth should stay relatively strong in the near term, albeit below last year’s levels.

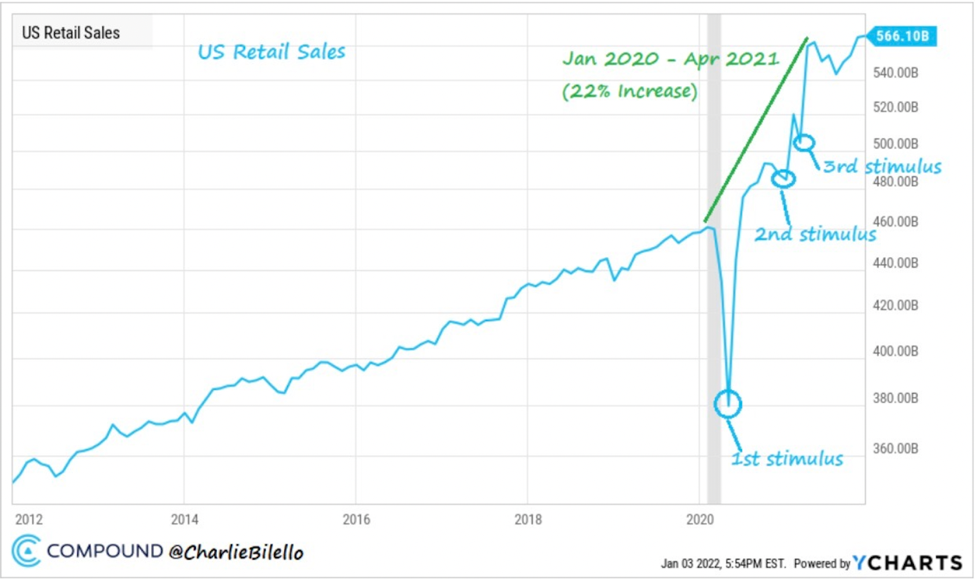

The longer-term economic picture is cloudier. Fiscal spending is declining from extraordinary heights. Charlie Bilello, founder and CEO of Compound Capital Advisors, notes that government stimulus helped retail sales surge 22% above pre-COVID levels in just 15 months between January 2020 and April 2021— greater sales growth than in the previous five years combined.

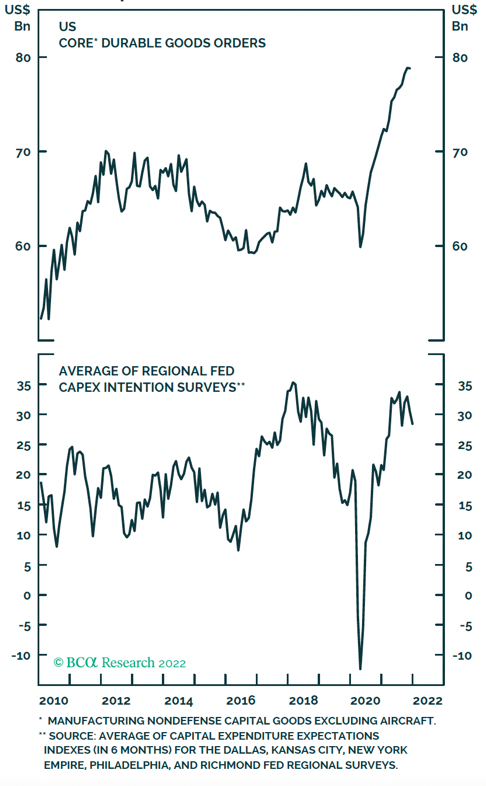

Now many pieces of the stimulus are expiring and Build Back Better is stalled, if not dead. David Rosenberg of economic consulting firm Rosenberg Research & Associates estimates that the withdrawal of stimulus alone will reduce U.S. GDP growth by three percentage points this year. Nevertheless, a number of factors could support ongoing economic growth, including the wealth effect from high stock and real estate prices and an increase in corporate capital expenditures as companies look to boost capacity to meet consumer demand.

Although omicron is likely to weigh on the economy in the short term, consumer spending may be a greater concern. Savings rates are down to 7.3%, below where they were at the start of the pandemic, and the childcare tax credit is ending for 35 million people. Weak retail sales point to flagging demand at the same time industrial production has increased. Mike Wilson, chief investment officer for Morgan Stanley, writes, “While omicron is part of the concern in the near term for certain activities, we are more focused on the risk of supply picking up just as consumption is fading.”

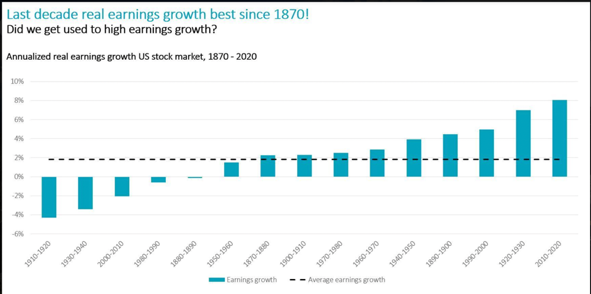

Facing slowing growth and higher wages, many companies may struggle to maintain the fast earnings growth of the past decade. The 20-teens had the strongest earnings growth of any decade in more than a century, helping to explain the equity market’s outsized gains. Corporate profits, like stock market returns, have tended to revert to the long-term mean. Historically, they haven’t boomed two decades in a row, and strong decades often have preceded weak ones. (The second-best decade for profit growth was the 1920s.)

POSITIONING: A TIME FOR CONSTRUCTIVE CAUTION

It’s clear to us that our position on the playing field has changed due to high inflation and the decided shift in Fed policy. Moreover, the effects of those trends are complicated by COVID-19 and all the related strains on the economy, including likely declines in globalization and revamping of supply chains.

The Fed may be becoming more hawkish just as inflation and demand peak and the economy slows, in which case tightening too aggressively could cause a recession. That outcome is far from certain; the economy may be able to weather higher rates, and the Fed might change course if inflation softens. Regardless, risk has risen.

Meanwhile, equity benchmarks are expensive and unlikely to maintain the kinds of powerful returns they’ve generated since 2009. Based on current valuations, it looks more realistic to expect long-term annualized returns in the neighborhood of 5%, probably lower for U.S. large-cap growth stocks. In the shorter term, the risk of a significant correction has increased considerably.

Despite this mixed outlook, in our view equities remain attractive relative to bonds for long-term investors. Stocks historically have fared well during most inflationary periods. And although cap-weighted equity benchmarks are expensive, the Fed’s signaling has taken a lot of the air out of the priciest parts of the market without a single rate increase.

We think inflation may moderate but stay higher than average. That scenario could improve the economy’s long-term growth outlook and lead to a steeper yield curve, potentially benefiting value stocks. We believe that backdrop and the enormous dispersion in the market present opportunities for skilled, value-conscious investors who know their portfolio businesses well. We are emphasizing strategies that employ managers who we believe have those qualifications, including long-short funds for appropriate portfolios.

We seek to maintain broad diversification in our portfolios, including exposure to small cap, international and emerging market equities. These asset classes provide important long-term portfolio benefits, and we believe they currently are attractive relative to large-cap U.S. stocks. History suggests that the beginning of a Fed tightening cycle may be accompanied by a weaker dollar, which could benefit equity markets outside the United States.

With bonds offering low income and presenting high interest-rate risk, we continue to seek other ways to generate income and diversify away from equities. We currently view positions such as Treasury inflation-protected securities (TIPS) and convertible arbitrage strategies as having the potential to deliver on those goals. In certain portfolios, we also continue to favor core cash-producing real estate opportunities, with a focus on the industrial and multifamily sectors. Demand for these property types is resilient, helping support high occupancy rates. These investments offer the potential for stable yield and a degree of inflation protection. We also are seeking to expand our exposure to industrial properties outside of the United States, where penetration rates are lower and the demand for new warehouses remains strong.

In our last issue we mentioned that we were investing in a distressed assets strategy for qualified portfolios. We also are investigating an investment in a strategy that focuses on distressed real estate. Current conditions are forcing over-leveraged property owners to sell attractive properties at attractive prices. In addition, we are exploring strategies that take sophisticated approaches to harvesting capital losses, helping to minimize the impact of taxes on investment returns.

All of these strategies reflect our commitment to serious investing. Right now, serious investing means recognizing that the market has shifted into a new phase—one that calls for caution and discipline.

LVW NEWS

Awards and Accolades

LVW Advisors CEO and Founder Lori Van Dusen, CIMA, has been named to the Rochester Business Journal’s 2021 Power 30 Banking and Finance list.

This year’s list honors financial services professionals who have worked for the past 20 months to aid the Rochester business community in navigating what have been murky and uncertain financial circumstances due to COVID-19.

According to the RBJ, the people on this year’s list have helped keep local businesses operating and advised them on new regulations and investment opportunities through the pandemic.

Congratulations to Lori!

View the full Power 30 Banking and Finance list here >

Click here for important disclosures regarding these awards.

Staying Current

LVW Advisors CEO and Founder Lori Van Dusen, CIMA, spoke with ETF.com about fixed-income alternatives for investors looking for yield in a low-interest-rate environment.

In our “Fourth Quarter State of the Markets” video, Joseph Zappia, CIMA, CCO/Co-CIO, and Jonathan Thomas, CFP , Private Wealth Advisor, discussed third quarter asset class returns, how inflation was impacting the market, and their overall perspective on investing at the time.

Lori Van Dusen, CIMA, recently spoke with Financial Advisor magazine about the Great Resignation.

Read the story to learn the options companies have for getting the work done while ensuring they are finding the right candidates for open jobs.

LVW Advisors Whitepapers

Preparing for Rainy Days: The Potential Role of Gold in Investment Portfolios: Gold can be a risk management tool for a well-balanced investment portfolio. The research team at LVW Advisors recently wrote a whitepaper outlining gold’s potential portfolio role, its inherent risks, the historical context of gold’s performance in stressed environments and ways investors can access the opportunity set.

Responsible Investing: Doing Good While Doing Well: The topic of responsible investing has recently garnered a lot of attention. While it may be referred to by various names, such as socially responsible investing; environmental, social and governance; diversity, equity and inclusion; and sustainable investing, we believe all of these references belong under the broader heading of responsible investing. The whitepaper provides more information on responsible investing and how a client can identify the issues important to them and reflect these views within their portfolio.

Bitcoin: The Potential Role of Digital Assets in Investment Portfolios: Bitcoin and other Digital Assets have been a hot topic in mainstream and financial news over the past several years. However, there is a high level of misunderstanding when it comes to the conversation around Digital Assets, by both financial professionals and everyday investors alike. In our view, the bulk of the misunderstanding and confusion around Bitcoin and other Digital Assets stems from preconceived notions based on both bearish misinformation and overidealistic views of the future. We believe that the reality, per usual, lies somewhere in the middle.

Our educational whitepaper provides some background of Digital Assets as well as the potential benefits and risks. Please be advised that LVW is not recommending an allocation to Digital Assets at this time, but continues to monitor and evaluate the opportunities that may exist.

On the LVW Advisors Blog …

Enjoy reading the latest LVW blog posts below.

SALT Proposal Gives Windfall to Top Earners in High-Cost Areas >

Employee News

Rachel Atkinson joined the LVW team in November as our Client Service Associate.

Rachel comes to us from Schwab where she serviced the LVW account. She has vast financial operations experience and we’re thrilled to have her on the team!

Originally from Atlanta, Georgia, Rachel and her husband and their Labrador retriever now live in Orlando, Florida. She and her husband love the outdoors, theme parks and University of Georgia football.

Welcome, Rachel!

Cheryle Kulikowski joined the LVW team in November as Lori Van Dusen’s Executive Assistant.

Prior to LVW, Cheryle held positions as a CPA at PricewaterhouseCoopers and various vice president roles at Citibank and Fleet Investment Services. She comes to us with robust experience that we are happy to have!

She and her husband live in Pittsford, New York, and have two sons.

Welcome, Cheryle!

Newsletter Citations:

1 Morgan Stanley Weekly Warm-Up, January 10, 2022.

2 Bloomberg, January 6, 2022.

3 Bloomberg, December 22, 2021.

4, 5 Standard & Poor’s, December 2021.

6 Wall Street Journal, January 6, 2022.

Disclaimer: This report is provided by LVW Advisors for general informational and educational purposes only based on publicly available information from sources believed to be reliable. Investing involves risk, including the potential loss of principal. Past performance may not be indicative of future results, as there can be no assurance that the views and opinions expressed herein will come to pass. No portion of this commentary is to be construed as a solicitation to effect a transaction in securities, or the provision of personalized tax or investment advice. Certain of the information contained in this report is derived from sources that LVW Advisors, LLC (“LVW” or the “Firm”) believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made. Indices are unmanaged vehicles that serve as market indicators and do not account for the deduction of management fees and/or transaction costs generally associated with investable products. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. The information in these materials may change at any time and without notice. Past performance is not a guarantee of future returns.

LVW is an SEC-registered investment advisor that maintains a principal office in the state of New York. This registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. The Firm may transact business only in those states in which it has filed notice or qualifies for a corresponding exception from applicable notice filing requirements. Additional information about LVW is contained in the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov.