67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

67 Monroe Avenue, Pittsford, NY 14534 / 9am - 4pm M-F

Welcome to the fall edition of LVW’s The Serious Investor.

In the third quarter, stronger-than-expected economic growth led investors to recalibrate their expectations for Federal Reserve policy, contributing to muted stock returns and weakness in bonds.

Forecasters increased their estimates of third-quarter GDP growth. The economy added almost 800,000 jobs during the quarter, and unemployment ended the period at 3.8%. That said, the headline jobs report can be deceiving, and certain underlying trends suggested softening in the job market. For example, according to the U.S. Bureau of Labor Statistics, the economy added more than 1.1 million part-time jobs but lost 692,000 fulltime jobs in the quarter. A cooling job market is good news for the fight against inflation.

Year-over-year inflation had come down to 3.2% as of July but rose to 3.7% in August. That increase, a strongerthan- expected economy and a rise in oil prices, led to renewed concerns that future inflation might force the Fed to extend its tightening campaign longer than anticipated. The Fed raised interest rates a quarter-point in July and left interest rates unchanged at its September meeting but indicated it might raise rates further in the coming months. (After quarter-end, however, Federal Reserve officials talked down the likelihood of another hike as financial conditions tightened.)

Complicating matters, several factors clouded economic projections, including a major autoworkers strike and the resumption of mandatory student loan repayments. And although Congress at the end of the quarter narrowly avoided a government shutdown, a potential shutdown looms when the current funding agreement expires in November. Geopolitical tensions, including war between Israel and Hamas, also are weighing on market sentiment.

The big story in the third quarter was the bond market. Investors adjusted their expectations in anticipation of interest rates staying higher for longer. This shift led to large-scale selling of longer-dated U.S. Treasury securities. The yield on 10-year Treasury notes rose from 3.84% to 4.58%, and the 30-year Treasury bond yield rose from 3.86% to 4.69% during the quarter. Yields on shorter-term bonds rose less, causing the yield curve to flatten. When rising long yields cause an inverted yield curve to flatten, bond investors call the dynamic a bear steepening—and historically it has been a harbinger for recession. Meanwhile, the U.S. dollar strengthened and oil prices jumped, as production cuts by Saudi Arabia and Russia pushed the price of a barrel of crude oil from roughly $70 to start the quarter to more than $90 at the end of September.

Energy was the top-performing sector, and dividend payers held up better than non-dividend-paying stocks as the market declined. U.S. stocks on the whole vacillated between modest gains and modest losses. The S&P 500 ended the quarter with a -3.6% return, outperforming most developed international markets.

Portfolios using the traditional 60/40 approach faced challenges in 2022, and in recent weeks the reemergence of a positive stock-bond correlation challenged them again. The correlation between stocks and bonds is heavily influenced by the level of interest rates; in higher rate environments the correlation tends to be positive, and vice versa. This means that bonds may not protect equity portfolios the same way they have over much of the last 20 years.

Our investment discipline considers markets through the lens of valuation, growth and liquidity. Our analysis leads us to the following conclusions as of early October:

Valuation: Equities are not overly expensive, and fixed income looks attractive

Equity: Excluding the 10 largest stocks in the S&P 500, stocks are trading near their 10-year average valuation, based on the price-to-earnings ratio—on the pricey side but not as expensive as the broad index would imply. Equity valuations are more attractive outside the U.S.

Fixed income: The Bloomberg U.S. Aggregate Bond Index currently yields 5.6% with a duration of six years, offering an attractive balance of risk and reward for fixed-income investors. Historically, a bond portfolio’s starting yield produces approximately 90% of its total return.

Growth: Earnings poised to recover

Wall Street Consensus leads us to believe that earnings bottomed in the second quarter, while earnings growth is projected to exceed 10% in 2024. Growth outside the U.S. is more subdued but generally positive.

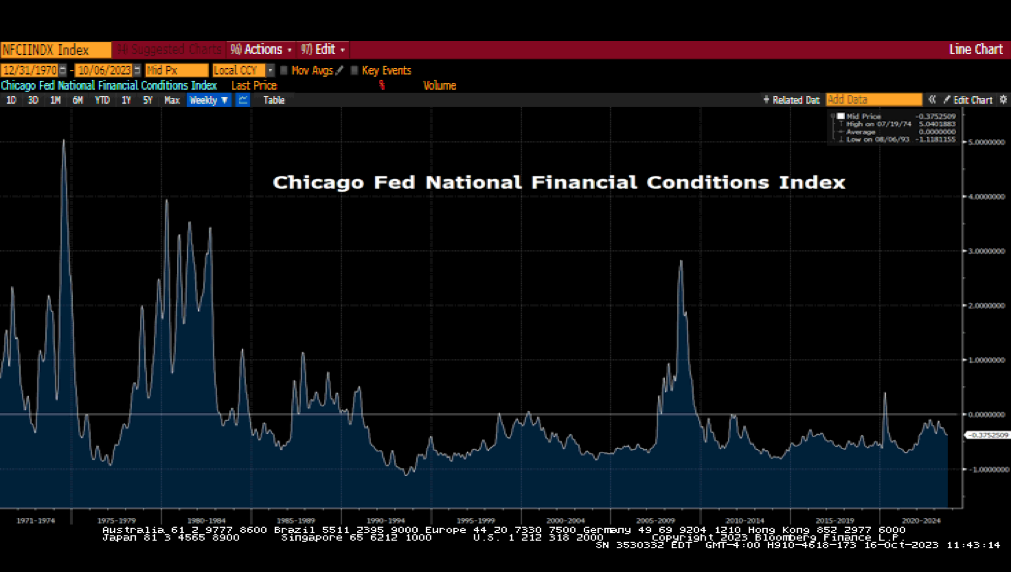

Liquidity: Tightening continues

The Fed continues to reduce its balance sheet, money supply continues to contract and higher interest rates have dramatically slowed credit creation. These developments are all consistent with the Fed’s mandate to bring inflation back to 2% by slowing economic activity. A longer-term view suggests today’s financial conditions are not tight by historical standards.

Summary

Low unemployment, moderating inflation, positive earnings and GDP growth, and reasonable valuations are, we believe, a positive setup for equities, provided the U.S. avoids recession.

Generally, throughout our client portfolios, we remain invested, overweighting areas that we believe offer more attractive valuations and a stronger margin of safety. The so-called Magnificent Seven have returned 92% on average this year, driving almost all of the return of the capitalization-weighted S&P 500 index. The rest of the S&P 500 trades at what we believe to be a more reasonable valuation multiple of 16-17x. Within our fixedincome allocations, we continue to favor short-duration, high-quality government and municipal issuers and reduced interest rate sensitivity as the yield curve continues to normalize.

We appreciate your continued trust and confidence in LVW.

Download a copy of this newsletter

Disclaimer: This material is provided by LVW Advisors (“LVW” or the “Firm”) for general informational and educational purposes only. Investing involves risk, including the potential loss of principal. Past performance may not be indicative of future results, and there can be no assurance that the views and opinions expressed herein will come to pass. No portion of this commentary is to be construed as a solicitation to effect a transaction in securities, or the provision of personalized tax or investment advice. Certain of the information contained in this report is derived from sources that LVW believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made. Indices are unmanaged vehicles that serve as market indicators and do not account for the deduction of management fees and/or transaction costs generally associated with investable products. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. The information in these materials may change at any time and without notice.

LVW is an SEC-registered investment advisor that maintains a principal office in the state of New York. This registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the adviser has attained a particular level of skill or ability. The Firm may transact business only in those states in which it has filed notice or qualifies for a corresponding exception from applicable notice filing requirements. Additional information about LVW is contained in the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov.